Waterhouse VC is a fund for wholesale investors, specialising in global publicly listed and private businesses related to wagering and gaming.

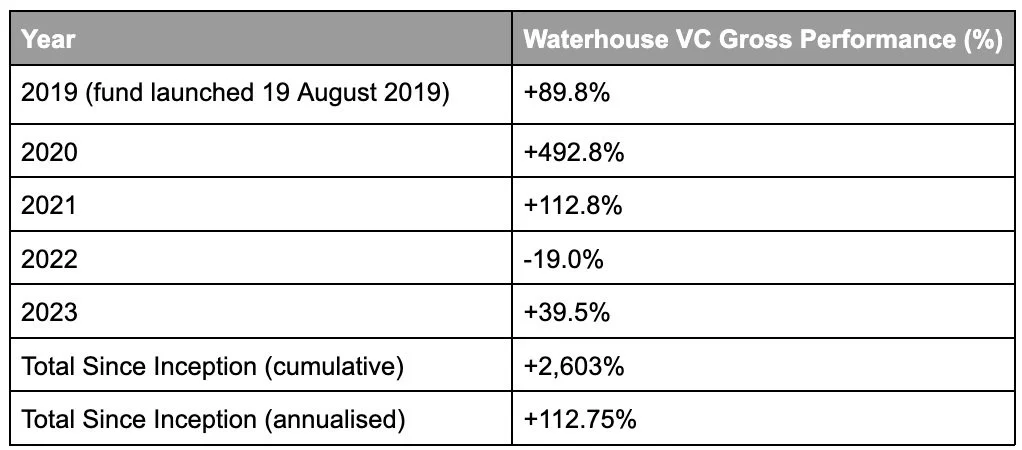

Since inception in August 2019, Waterhouse VC has achieved a gross total return of 2,603% as at 31 December 2023, assuming the reinvestment of all distributions.

A year in review

In 2023, Waterhouse VC generated a strong return of +39.5%, strongly outperforming the S&P500 (+24.8%) and the ASX200 (+7.8%).

Waterhouse VC’s gross performance, as at 31 December 2023.

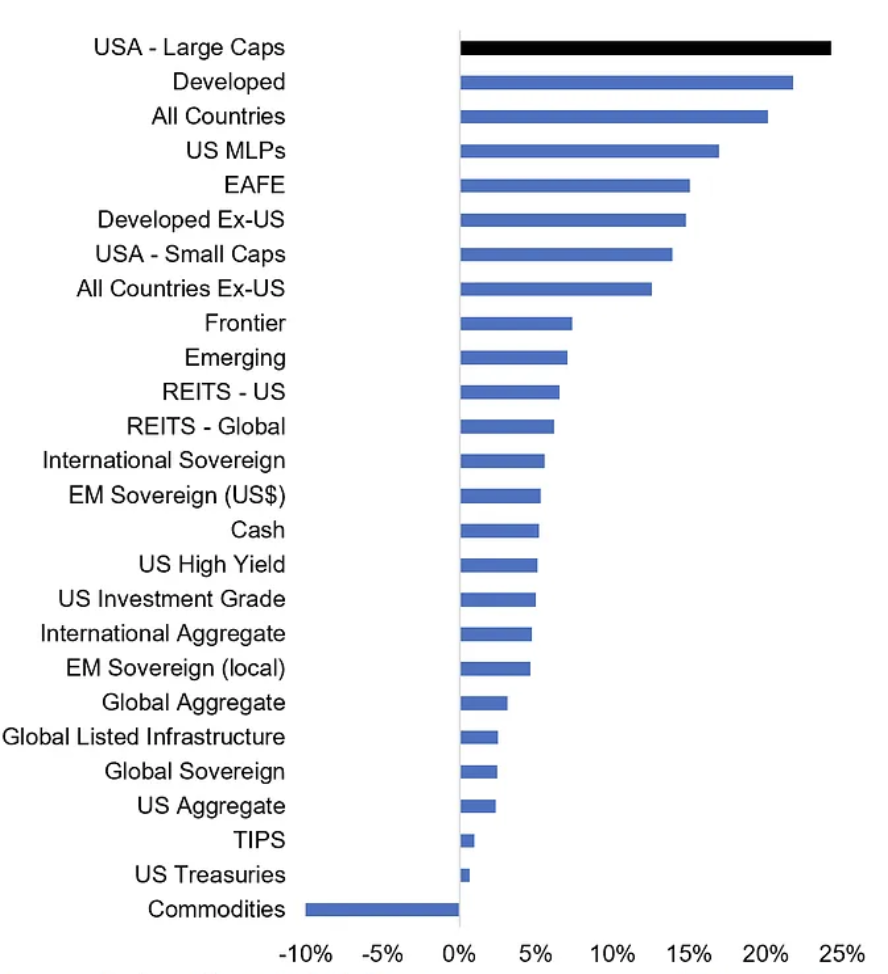

Whilst company valuations broadly increased in 2023, there was significant divergence across geographies and sectors. With the increase in interest rates globally, investors have grown more selective, preferring to invest in profitable businesses. Portfolio Manager, Peter Stevens, discussed this phenomenon at iGaming Next in Malta, with reference to the gaming and wagering industry (watch here).

Performance of various asset classes and sectors in 2023. Source: Topdown Charts, Refinitiv Datastream

In 2023, there were two stand out contributors to the fund’s +39.5% performance:

Project Tennis - a professional betting syndicate founded by Tom Dry focused on tennis (first discussed in December 2022 and invested in on 1 July 2023)

Saintly - a crypto wagering operator and B2B platform (see more here) - position exited in August 2023.

Beating the house

We are very pleased with the operational performance of Tom Dry’s betting syndicate going into 2024. The fund is on track to earn back in distributions its entire investment in the syndicate by January 2025, just 18 months after the investment was made. More broadly, professional betting is a key focus area for the fund and we are actively exploring several professional betting opportunities.

In addition to tennis, we are looking at other professional betting opportunities in horse racing, which is particularly interesting due to the rebates offered by totes. Large syndicates benefit from generous rebates in pari-mutuel/tote betting, thanks to their role in supplying liquidity. This gives them a significant advantage (which varies based on the tote pool) over other bettors. To qualify for these rebates, syndicates must wager substantial amounts of money. For example, US totes typically only grant rebates to those who wager over US$5 million per year (Sports Trading Network).

Emerging professional betting syndicates focused on racing are already behind the larger syndicates by a few percentage points because of the rebates that the larger syndicates receive. The accumulation of the rebate advantage has resulted in substantial and lucrative profits for the largest racing-focused syndicates. If Waterhouse VC could own a stake in a syndicate that bets on racing and receives rebates from the totes, that would be a very exciting portfolio holding.

Saintly - a seven month journey

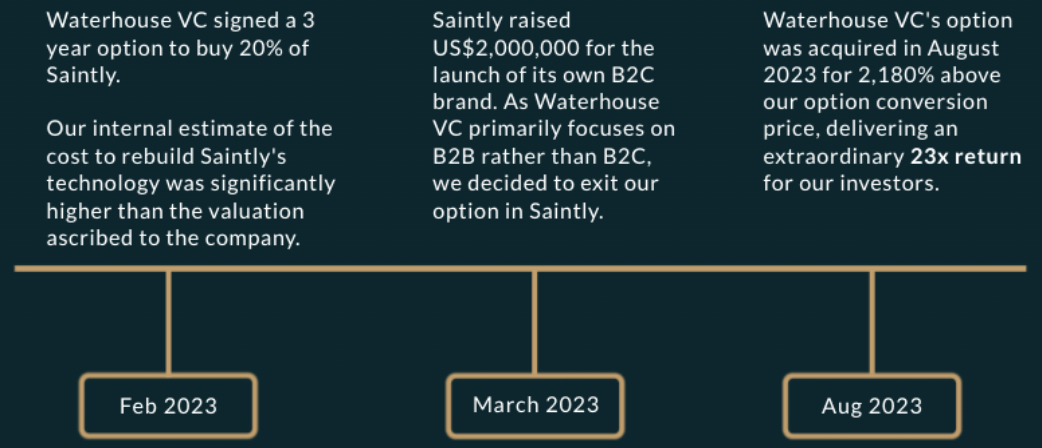

Saintly was the largest single contributor to the fund’s performance in 2023. We negotiated an option to buy 20% of Saintly in February 2023 because of its technology platform which positioned the company well to take advantage of the burgeoning opportunity in crypto wagering, which we first discussed in May 2022. Online crypto operators (such as Sportsbet.io and Stake.com), which have a similar UX to online fiat operators like FanDuel and DraftKings, are already recording extraordinary turnover.

The timeline below shows the history of Waterhouse VC’s option deal with Saintly from signing in February 2023 through to exiting in August 2023 for 23 times the option conversion valuation.

Timeline of Waterhouse VC’s involvement with Saintly

India and Brazil - emerging market opportunities

As we look forward to 2024, emerging markets such as Brazil (discussed here) and India (discussed here) will be key growth regions for both operators and B2B suppliers.

The online wagering industry in India is growing at over 20% per annum (Sportskeeda) and has been fueled by the country's rapid economic progress, with GDP per capita up 2x since 2009, and a substantial market size of over 370 million bettors (MyBetting India). Wagering turnover on cricket alone is estimated to be US$150 billion, with approximately 85% of Indian bettors engaging in cricket wagers (GiiResearch). The legal status of wagering in India remains grey in most areas.

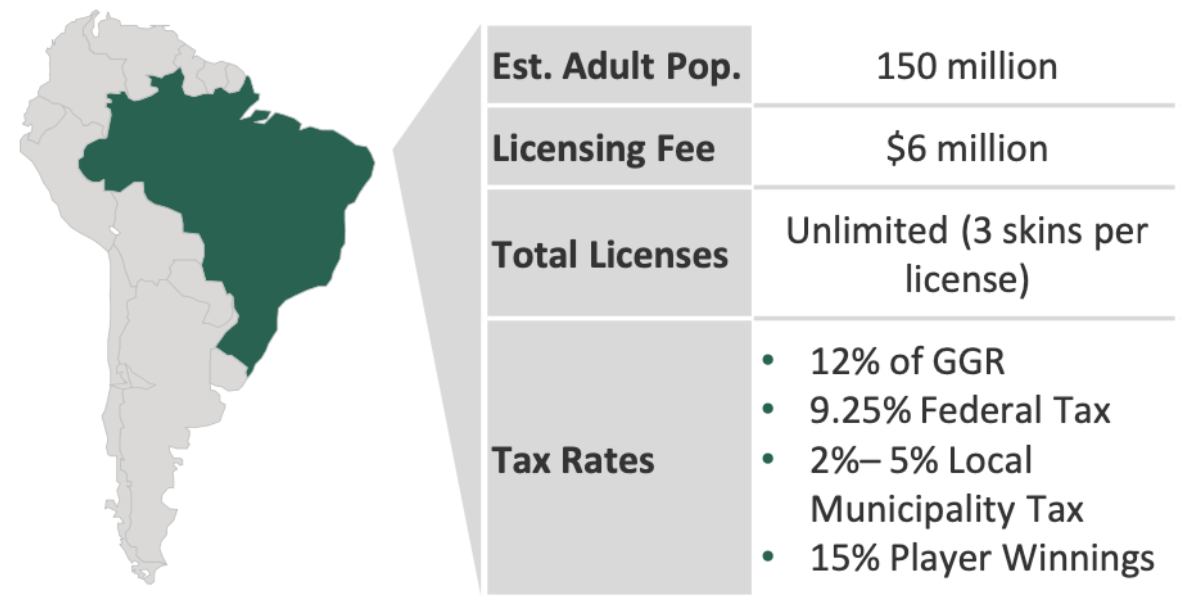

Brazil recently introduced online wagering following official approval from the country’s President Lula. Operators are anticipating the imminent launch of the newly regulated industry, with 134 operators having already signed pre-market ordinance measures (SBC News).

Brazil online wagering market statistics. Source: Citizens Capital Markets Research

Looking to 2024

We are particularly excited by professional betting, emerging markets such as Brazil and India, and B2B suppliers that provide a critical or truly unique service to gaming and wagering operators.

We have identified several companies in the industry currently valued attractively at just 1x revenue plus approximately their net cash on the balance sheet. We offer wholesale investors unique access to these larger deals, which remain at depressed valuations.

Media

I am speaking alongside Adam Rosenberg (Senior Advisor to Blackstone for Gaming & Leisure) at ICE London on the 7th of February about emerging wagering markets in Africa, Asia, and Latin America, as well as the remaining potential in the US and Eastern Europe. For more information on the event, see here.

I am also speaking on ‘Investing in the Innovation Gold Rush’ at SBC Summit Rio 2024. With Brazilian sports betting operators establishing themselves in the new market, the panel will discuss the opportunity for operators as well as the current investment landscape. For more information on the event, see here.

I recently joined Brad Allen on ‘Zero Latency: An Eilers & Krejcik Gaming Podcast’. We discussed why the fund is investing in betting syndicates, whether US sportsbooks should be forced to take minimum bets, and why voice betting could be a significant opportunity. Listen to the podcast here.

For wholesale investors interested in following wagering and gaming industry news and trends, please follow our updates on Twitter (@waterhousevc) or through our website at WaterhouseVC.com.

All the best,

Tom

DISCLAIMER AND IMPORTANT NOTES

Please note the above information in relation to Sportsbet.io, Stake.com, Flutter Entertainment Plc, DraftKings and Saintly is based on publicly available information in relation to the company and should not be considered nor construed as financial product advice. The above information in relation to Thomas Dry and Project Tennis is based on information provided by the company and should not be considered nor construed as financial product advice. The Fund currently has a position in Flutter Entertainment Plc and Project Tennis. The information provided in this document is general information only and does not constitute investment or other advice. Readers should consult and rely on professional investment advice specific to their individual circumstances.

General Information Only

This material is for general information only and is not an offer for the purchase or sale of any financial product or service. The material has been prepared for investors who qualify as wholesale clients under sections 761G of the Corporations Act or to any other person who is not required to be given a regulated disclosure document under the Corporations Act. The material is not intended to provide you with financial or tax advice and does not take into account your objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by Sandford Capital, Waterhouse VC or any other person. To the maximum extent possible, Sandford Capital, Waterhouse VC or any other person do not accept any liability for any statement in this material.

Financial Regulatory Oversight and Administration

Waterhouse VC is an Australian Unit Trust denominated in AUD and available to wholesale institutional investors worldwide with a minimum of AUD 1,000,000 or USD / EUR / GBP / JPY / CHF equivalent. This material has been prepared by Waterhouse VC Pty Ltd (ABN 48 635 494 861) (‘Waterhouse VC’, ‘Trustee’, ‘us’ or ‘we’) as the Trustee of the Waterhouse VC Fund (the ‘Fund’). The Trustee is a corporate authorised representative (CAR 1296688) of Sandford Capital Pty Limited (ABN 82 600 590 887) (AFSL 461981) (Sandford Capital) and appoints Sandford Capital as its AFS licensed intermediary under s911A(2)(b) of the Corporations Act 2001 (Cth) to arrange for the offer to issue, vary or dispose of units in the Fund.

Performance

Past performance of Waterhouse VC is not a reliable indicator of future performance. Waterhouse VC Pty Ltd does not guarantee the performance of any strategy or the return of an investor’s capital or any specific rate of return. No allowance has been made for taxation, where applicable. We encourage you to think of investing as a long-term pursuit.

Copyright

Copyright © Waterhouse VC Pty Ltd ACN 635 494 861. No part of this message, or its content, may be reproduced in any form without the prior consent of Waterhouse VC.

Governing Law

These Terms and Conditions of use are governed by and are to be construed in accordance with the laws of New South Wales. By accepting these Terms and Conditions of use, you agree to the non-exclusive jurisdiction of the courts of New South Wales, Australia in respect of any proceedings concerning these Terms and Conditions of use.