See below for this month’s Waterhouse VC newsletter. We specialise in global publicly listed and private businesses related to wagering and gaming.

Since inception in August 2019, Waterhouse VC has achieved a gross total return of 2,439% as at 31 October 2023, assuming the reinvestment of all distributions.

Not too hot, not too cold, just right

As with Goldilocks and porridge, so it is with gambling regulation/taxation. If it is too severe or too lax then Goldilocks will not participate in the regulated gambling industry.

Balancing gambling regulation/taxation is crucial to ensure a harmony between safeguarding consumers, thwarting criminal activities, and cultivating a market that is both fair and competitive. A well-crafted regulatory framework effectively considers the interests of betting operators, consumers, and the broader community.

If regulation/taxation is too severe then the following negative outcomes can occur:

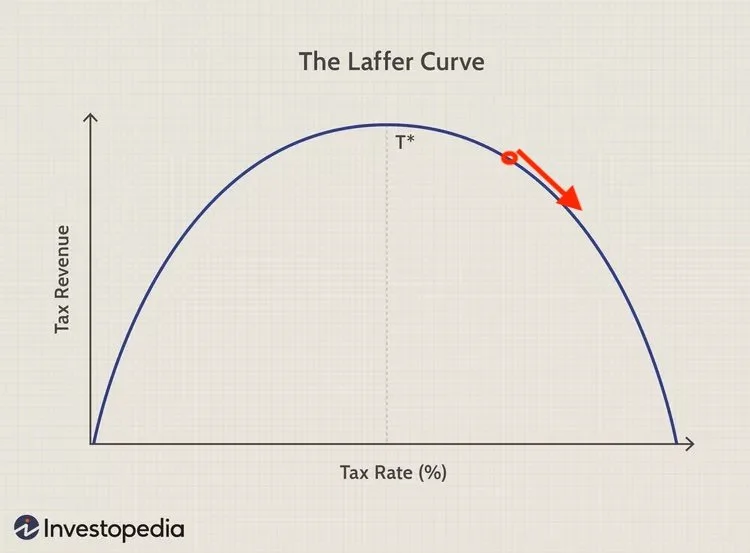

Laffer Curve

Focusing particularly on government tax revenues from wagering, the Laffer Curve illustrates the relationship between tax rates and government revenue, suggesting that there is an optimal tax rate at which government revenue is maximised. In the 1980s, the Reagan Administration used the Laffer Curve as rationale for implementing tax cuts.

Beyond the optimal tax rate, increasing tax rates may decrease tax revenue due to economic activity being disincentivized. When applied to the wagering industry, the Laffer Curve demonstrates that there is a point of maximum taxation at which it becomes no longer worthwhile to operate a regulated wagering business.

On the other hand, if tax rates on wagering activities are too low, the government may not collect as much revenue as required to cover the regulatory and social costs associated with wagering. Unlike other industries, if taxes are too high in the gambling industry, consumers are driven towards unregulated or illegal wagering operators, where consumer protection is not stringent.

The Laffer Curve (annotated by Waterhouse VC). In some regulated betting markets, it could be argued that we are past the point of maximum tax revenue and are now impacting tax revenue because the direction of taxation policy has been set. Source: Investopedia

Demand for betting has not dropped as taxation has increased. Consumers have simply sought other ways to bet, such as through offshore bookmakers, often licensed in jurisdictions such as Curaçao. According to the American Gaming Association’s (AGA) 2022 study "Sizing the Illegal and Unregulated Gaming Markets in the United States", it is estimated that Americans bet US$510.9 billion annually with illegal and unregulated operators. This results in a US$44.2 billion loss in gaming revenue for the legal betting industry and a US$13.3 billion decrease in tax revenue for state governments.

Government gaming taxes generated in 2021 and taxes lost to illegal and unregulated betting. Source: AGA.

Annual US gaming revenue across legal and illegal betting. Source: AGA.

Market sharing amongst few

Increased taxes create barriers to entry for new and smaller operators, whilst progressively squeezing out less competitive operators. Larger operators benefit from economies of scale, with operational costs, marketing and overheads spread across a large customer base.

Consequently, similarly to the tobacco industry, in most regulated wagering markets (such as Australia, the UK, France, Italy and the United States), the majority of market share is split amongst just a handful of operators, which negatively impacts consumer choice and ultimately, the consumer’s betting experience, as there is less pressure on operators to innovate and compete to retain customers.

In Australia, just one operator (Sportsbet, which is owned by Flutter Entertainment) has 41% market share. In Australia, the UK and France, the largest three operators collectively have over 60% market share. In the US, the largest three operators have 76% market share - they are FanDuel (owned by Flutter Entertainment), DraftKings and BetMGM.

Online sports betting market share split amongst the top 5 operators in highly regulated betting markets. Source: iGaming Business.

Trickling down

When looking at the Australian market, a general waterfall from revenue down to net profit for a large-scale operator would include:

GST - 10% of revenue (see more here)

Point of Consumption Tax - 15% of revenue (this varies by state - in New South Wales, it is 15%)

Race Fields Fee - 15% of revenue (estimate extrapolated from 1.5-2% fees on turnover)

A scale operator could feasibly spend 20% of revenue on marketing and 10% of revenue on operations. After corporate tax, this leaves a net profit after tax margin of 22.5%. In total, in this theoretical scenario, $47.50 in every $100 of betting revenue goes towards some form of tax.

Scale and operational leverage are achieved when marketing and operational costs form a smaller part of revenue, with cost efficiency and increased profit margins as fixed costs are spread over more customers. For operators that spend a large amount of money as a percentage of revenue on marketing and operations, it is not viable to operate in Australia.

Waterfall from revenue down to net profit after tax for a typical large-scale Australian wagering operator.

In Sportsbet’s most recent quarterly result, Flutter said that, “The market is also experiencing increased regulatory oversight, including a ban on credit card deposits”. The proposed credit card deposit ban in Australia exemplifies the other regulatory measures outside of taxation that are available to regulators.

Losing greys

Betting markets are typically split into three buckets: ‘white’ (regulatory framework is well-defined, such as the United Kingdom), ‘grey’ (regulatory framework is unclear, ambiguous or varies between states, such as India) and ‘black’ (regulatory framework consists of strict laws against betting, such as Saudi Arabia). We believe that the number of grey markets will shrink over time and there will be a clear split between white and black markets.

When investing in the wagering industry, our focus is on businesses that are well-equipped to navigate regulatory challenges. One of those survival tools is scale; whilst another is investing in the infrastructure of wagering rather than the operators themselves - Waterhouse VC directs its efforts towards this B2B infrastructure. When evaluating opportunities for the fund, we seek businesses that not only survive but also thrive under the pressures of taxation and regulation.

Media

I recently spoke with James Breslo on his podcast, ‘Double Down with Breslo’. Watch ‘Racing Dynasty to Investment Pioneer: Insights from Tom Waterhouse’ here.

For wholesale investors interested in following wagering and gaming industry news and trends, please follow our updates on Twitter (@waterhousevc) or through our website at WaterhouseVC.com.

All the best,

Tom

DISCLAIMER AND IMPORTANT NOTES

Please note the above information in relation to FanDuel, Sportsbet, Flutter Entertainment Plc, DraftKings and BetMGM is based on publicly available information in relation to the company and should not be considered nor construed as financial product advice. The Fund currently has a position in Flutter Entertainment Plc. The information provided in this document is general information only and does not constitute investment or other advice. Readers should consult and rely on professional investment advice specific to their individual circumstances.

General Information Only

This material is for general information only and is not an offer for the purchase or sale of any financial product or service. The material has been prepared for investors who qualify as wholesale clients under sections 761G of the Corporations Act or to any other person who is not required to be given a regulated disclosure document under the Corporations Act. The material is not intended to provide you with financial or tax advice and does not take into account your objectives, financial situation or needs. Although we believe that the material is correct, no warranty of accuracy, reliability or completeness is given, except for liability under statute which cannot be excluded. Please note that past performance may not be indicative of future performance and that no guarantee of performance, the return of capital or a particular rate of return is given by Sandford Capital, Waterhouse VC or any other person. To the maximum extent possible, Sandford Capital, Waterhouse VC or any other person do not accept any liability for any statement in this material.

Financial Regulatory Oversight and Administration

Waterhouse VC is an Australian Unit Trust denominated in AUD and available to wholesale institutional investors worldwide with a minimum of AUD 1,000,000 or USD / EUR / GBP / JPY / CHF equivalent. This material has been prepared by Waterhouse VC Pty Ltd (ABN 48 635 494 861) (‘Waterhouse VC’, ‘Trustee’, ‘us’ or ‘we’) as the Trustee of the Waterhouse VC Fund (the ‘Fund’). The Trustee is a corporate authorised representative (CAR 1296688) of Sandford Capital Pty Limited (ABN 82 600 590 887) (AFSL 461981) (Sandford Capital) and appoints Sandford Capital as its AFS licensed intermediary under s911A(2)(b) of the Corporations Act 2001 (Cth) to arrange for the offer to issue, vary or dispose of units in the Fund.

Performance

Past performance of Waterhouse VC is not a reliable indicator of future performance. Waterhouse VC Pty Ltd does not guarantee the performance of any strategy or the return of an investor’s capital or any specific rate of return. No allowance has been made for taxation, where applicable. We encourage you to think of investing as a long-term pursuit.

Copyright

Copyright © Waterhouse VC Pty Ltd ACN 635 494 861. No part of this message, or its content, may be reproduced in any form without the prior consent of Waterhouse VC.

Governing Law

These Terms and Conditions of use are governed by and are to be construed in accordance with the laws of New South Wales. By accepting these Terms and Conditions of use, you agree to the non-exclusive jurisdiction of the courts of New South Wales, Australia in respect of any proceedings concerning these Terms and Conditions of use.